Table of Contents

The HSA is one of the most amazing, efficient, and effective places to save your money for retirement. The irony is, it’s not even a retirement account! It has mind-blowing benefits that are fantastic for those who qualify.

As you will soon see the HSA is the most powerful savings account because it has triple tax savings. Let’s dig into the massive tax benefit of this super retirement account.

What Is A Health Savings Account (HSA)?

An HSA is simply a savings account. Yet it can do so much more than regular savings account that you open at your local bank.

Think of a normal checking or savings account but with a slew of benefits.

To qualify for an HSA you must have a high deductible health plan. People who have high deductible health plans will face high out of pocket costs, due to their higher deductibles. So, the government provides tax incentives to motivate people to actually save for their health expenses.

If you are unfamiliar with high deductible health plans, don’t worry, I’ve got your back.

High Deductible Health Plan (HDHP)

To reap the amazing benefits of an Health Savings Account, you must have a High Deductible Health plan (many times called an HDHP).

If you don’t know what a deductible is, let me break it down simply. It is the amount of money you have to pay out of pocket before your insurance kicks in.

For example, if you have a $2,500 high deductible health plan, you must pay $2,500 out of pocket first, before your insurance will pay the rest.

You may also hear other terms thrown around like a premium. Your premium is not the same as a deductible. Understanding your premium is simple, it is just the amount you pay each month for your health insurance.

Your premium in a HDHP will be lower since the deductible is higher.

A high deductible health plan may not be for every person, in every situation. But it can make sense for a lot of people. If you have no earthly clue whether or not you have an HDHP, just reach out to your HR department (or insurance rep if you are self-employed) and they can tell you.

How Most Retirement Accounts Work

Most retirement accounts have great tax benefits and you should definitely be taking advantage of them. But none can compare to the HSA. Let’s take a look at why that is.

The 401(k) or Traditional IRA Tax Benefits

The 401(K) or traditional IRA are pre-tax contributions. This means that these accounts allow you to contribute without paying taxes on those contributions.

For example, if you make 100K per year, and you contribute $10,000 into a 401(k), then the government only considers you making $90,000 that year.

That’s not all folks. When you invest your money in these accounts, it also grows tax-free. Another massive benefit!

Here is how it looks visually:

The ROTH IRA Tax Benefits

The Roth IRA is slightly different than the 401(K). With a Roth IRA, you pay taxes as you contribute to your account. But, this money grows tax-free, and you do not have to pay taxes when you take the money out.

This means you can watch your pile of money grows without paying taxes. So if you make $100,000, the IRS will still consider you making a hundred grand if you contribute to a Roth. But, you can pull that money out (at age 59.5) tax-free.

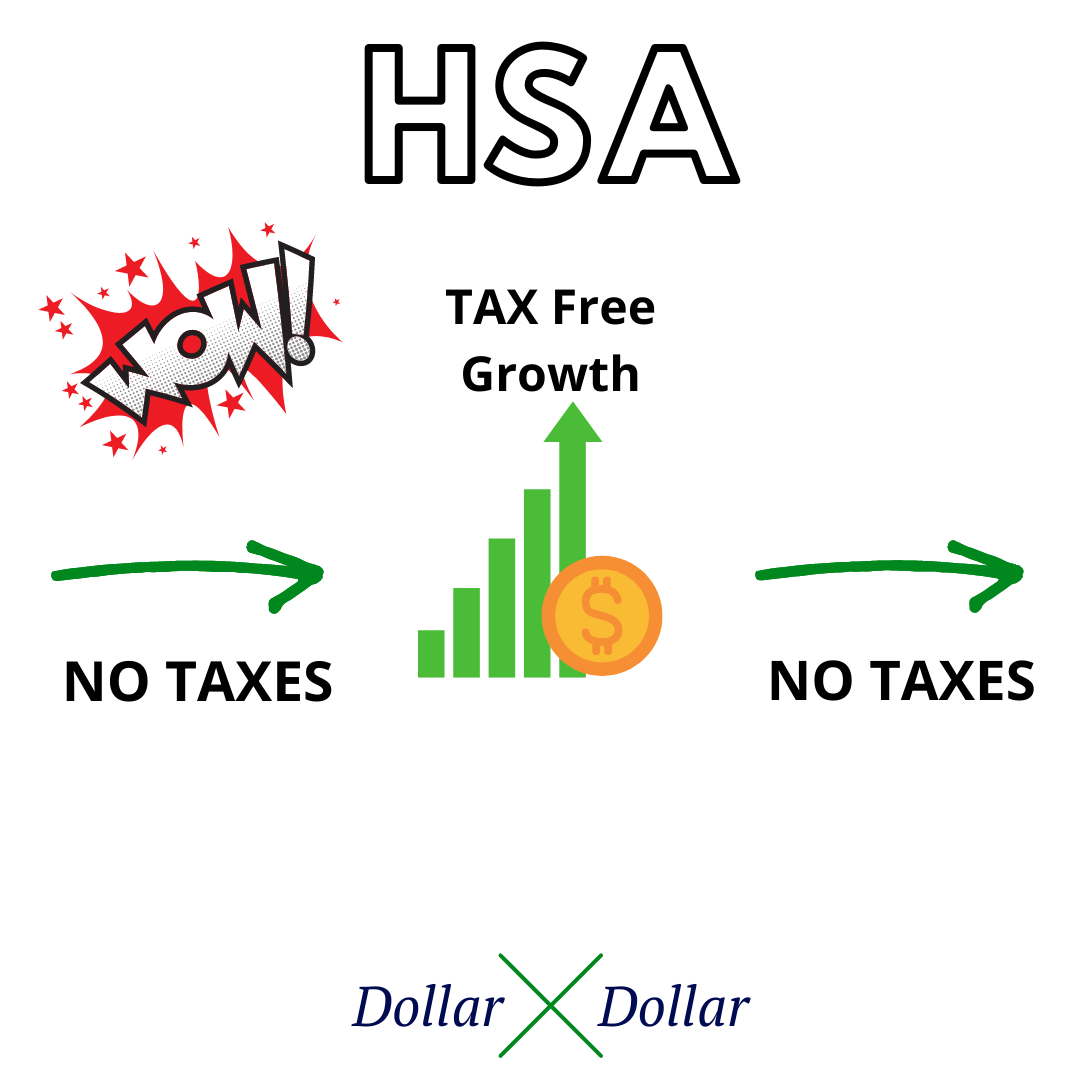

Health Savings Account (HSA) Tax Benefits

For the HSA we have the best of both worlds. What most people do is they contribute to their HSA as a savings account for their healthcare. That is all fine and dandy. But, I want you to ignore the healthcare part since we are trying to optimize our tax savings.

We want to go against the grain and find those financial hacks right?

The HSA allows you to contribute to your account tax free, it grows when invested tax free, and you can withdraw the money tax free! This is a triple tax savings!

The best part is, you can take this money out whenever you want. You don’t have to wait for retirement to or pay a penalty like the Roth and 401(k).

As long as you have a qualified medical expense after the account was opened, you can pay yourself whenever you want. That means the money you contribute to your HSA is yours forever.

HSA Contribution Limits

For the year 2021, the HSA contribution limits are $3,600 for someone on an individual plan. If you are on a family plan the contribution limits for 2021 are $7,200.

If you have any family members (husband, wife, children, other dependents) on your plan, you will more than likely qualify for the family plan contribution.

Delaying Your HSA Distributions For the Future

There is no rule as to when you need to pay yourself for a medical expense with an HSA. You can defer all your medical expenses until a later date. Then, reimburse yourself whenever you retire (or whenever you want).

The key here is to make sure that the medical expense occurred after the account was opened. If it was not, then that expense will not be eligible.

The HSA Tracking System

To put this system into a place you must be organized. Keeping track of all your medical receipts over time so that you can reimburse yourself can be tedious. That is why keeping digital copies is the best system. Here is what I do:

- Receive medical bills or receipts.

- Scan it into my computer/mobile app with my phone.

- Save the receipt in a cloud service like OneDrive or Dropbox. This allows you to ensure that you can access the receipts wherever you go.

- Add the date/amount to a spreadsheet to track my total. The spreadsheet keeps a running total so you know how much reimbursement you have available.

How Much Can My Health Savings Account Grow?

The amazing thing about your HSA is that you can invest the money you contribute. Let’s say you max out your HSA for 30 years with a family plan. You invest in an index fund that returns 8% over those 30 years. At the end of 30 years, you will have $804,310.00.

| Year | HSA Amount |

| 1 | $7,100.00 |

| 5 | $41,652.87 |

| 10 | $102,854.59 |

| 15 | $192,780.01 |

| 20 | $324,909.95 |

| 25 | $519,052.17 |

| 30 | $804,310.80 |

Or if you have an individual plan where you can invest $3,600.00 a year and invest for 30 years, you are looking at $407,819.56.

| Year | HSA AMOUNT |

| 1 | $3,600.00 |

| 5 | $21,119.76 |

| 10 | $52,151.62 |

| 15 | $97,747.61 |

| 20 | $164,743.07 |

| 25 | $263,181.38 |

| 30 | $407,819.56 |

What if I have too Much Money in my HSA?

After you see how much your money can grow over time, you may be thinking to yourself, what if my bank roll is too big in my HSA when I am ready to use it? After all, that would take a lot of medical receipts.

Well, if you are a generally healthy person and do not have enough medical bills to cover the amount of money you have, first of all celebrate. Having too much money is a great problem to have.

Secondly, don’t worry at all. The HSA will work just like a traditional IRA. The only difference is that your withdrawal year will move to 65 instead of 59.5.

Just like the traditional IRA or 401(K), your money will grow tax free, then you will just have to pay income tax when you take your money out of the HSA (for any withdrawals that do not have a medical expense).

So, your HSA is almost exactly the same as an IRA except all those medical expenses are tax free!

Other Massive HSA Benefits

There are a number of other benefits to an HSA including:

Employer Match

Some employers will offer an HSA match. As you know, I am a huge fan of free money, so make sure you take advantage of this. Ask your HR department if they offer this option.

Contribute Through Your Employer or Payroll Deduction If Possible

If you contribute through your employer via automatic payroll deduction, you can save on more taxes. This means that if you contribute right out of your paycheck you can save on social security and medicare taxes which is another 7.5%!

Invest the Money

Don’t let your money sit in an HSA without working for you. Make sure you reap the benefits of compound interest and consider investing in low cost index funds. Be mindful that you aren’t in some high fee actively managed funds that will eat away at your gains.

What Qualifies as a Medical Expense by the IRS?

Here a list of common medical expenses you can reimburse with an HSA. This is not an all-inclusive list. Make sure you check out irs.gov for the full list as it is always changing. Publication 902 and 569.

• Acupuncture

• Alcoholism treatment

• Ambulance

• Artificial limbs

• Artificial teeth

• Breast reconstruction surgery

(mastectomy-related)

• Chiropractic services

• Cosmetic surgery (only if due to

trauma or disease)

• Dental treatment (X-rays, fillings,

braces, extractions, etc.)

• Diagnostic devices (such as blood

sugar test kits for diabetics)

• Doctor’s office visits and

procedures

• Drug addiction treatment

• Eyeglasses, contact lenses and eye

exams

• Eye surgery (such as laser eye

surgery or radial keratotomy)

• Fertility enhancements

• Hearing aids (and batteries for use)

• Hospital services

• Laboratory fees

• Long-term care (for medical

expenses and premiums)

• Menstrual care products

• Nursing home

• Nursing services

• Operations/surgery (excluding

unnecessary cosmetic surgery)

• (Certain) over-the-counter drugs

and medications

• Physical therapy

• Prescription medicines or drugs

• Psychiatric care

• Psychologist counseling

• Speech therapy

• Stop-smoking programs

• Vasectomy

• Weight-loss programs (must be to

treat a specific disease diagnosed

by a physician)

• Wheelchairs

• X-rays

Andrew is the host of The Personal Finance Podcast, a show that is changing the way you think about your money. His primary goal with the podcast is to bring as much value as possible to his listeners.

Andrew's favorite free financial tool he's been using since 2014 to manage his net worth is Personal Capital. Each month he uses their free Investment Checkup tool and Retirement Planner to track his investments and ensure that he's on the fast track to financial freedom.

His favorite investment platform is M1 Finance, a site that allows him to build a custom portfolio of stocks for free. It has no trading fees and is his preferred way to invest without having to lift a finger.

- Who is Eligible for an FHA Loan? - November 10, 2020

- How to Write a Check: A Step by Step Guide (With Examples) - November 6, 2020

- How to Buy Vanguard Index Funds - October 14, 2020