Table of Contents

You may be realizing that you need to start saving for retirement. But, there are a ton of options out there.

The 401(k) is a wonderful way to save for retirement. In fact, the number of 401(K) millionaires has reached an all-time high.

Surging markets and a booming economy may have something to do with it. But, the many Americans who have achieved the impressive million-dollar club, also have practiced sound personal finance principles.

The key is to understand that you can do this too. The recipe is simple. Time, discipline, and consistency are how you get there.

Most 401(k) millionaires don’t have anything special. In fact, they are usually millionaires next door. Their outward appearance would never show it.

You may never know how much wealth they’ve built unless you took a peek at their statement.

How to Become a 401(k) millionaire

Becoming a 401(k) millionaire is not out of the question. A growing number of Americans have already done it. The key is to consistently invest over a long period of time.

Why? Because you are limited in the amount of money you can invest in a 401(K).

You can never get the time you lost back. So maximizing the amount you throw at your 401(k) each year is very important. Here are a few tips to get the most out of your 401(k)

Start Investing Early In Your 401(k)

The earlier you begin investing, the sooner compound interest will get to work for you.

In fact, if you start investing at age 25 instead of age 35. You will have to contribute much less than the late starter to reach a million dollars.

Investing in your 401(K) early matters. In fact, it’s a game-changer.

Longevity is the name of the game in retirement accounts. You can’t expect to invest for a handful of years and come out the other side a millionaire. It takes a decade or two to really get the ball rolling.

Invest in Low-Cost Investments like Index Funds or Target Date Funds

Index funds are a great way to invest for retirement with a minimal expense ratio. Some index funds now have a 0% expense ratio!

Having high investment costs will really add up in the long run. In fact, for someone who maxes out a 401(k), a 1% expense ratio could cost you 6 figures!

Always look at the expenses of each fund. As a rule of thumb aim to keep your expense ratios below .50 or less (50 basis points).

If it’s anything higher you are likely getting ripped off with no added benefit.

VTSAX is my favorite 401(k) investment. You are buying the entire stock market in one index fund.

It allows you to grab every piece of the pie while not having to worry.

Always Get Your Employers Match

If you are not getting your employers match, then you are not taking advantage of an amazing benefit. You are actually leaving free money on the table. That’s right, free!

Say for your example your employer will match 3% of every dollar you contribute to your 401(k). All you have to do is contribute 3%.

If you don’t contribute, you are saying that you don’t want to double your money. That is ludicrous.

If you are lucky enough to work for an employer who offers a match. Always take it.

Try to Max Out Your 401(K) When You Can

The amount you can contribute to your 401(k) is constantly going up. Currently, you can invest $19,500 per year. If you are over the age of 50, you can contribute even more as a catch-up contribution. The catch-up contribution is $6,500.

If you can max out your 401(k) in your early years you will have a massive advantage.

When money is invested early on it compounds. That money creates new money, which will create even more money in the future.

This starts to pile up. It builds. It begins to swell.

It’s truly exciting to watch your 401(k) grow.

In the early years, you may feel like you’re not getting far. But as time goes on you will see it accelerate. In fact, just know that the first 100k is a slog.

It takes forever for your 401(k) to hit that point. But, once it does, you are going to see the growth begin to speed up.

Then, once you hit a few hundred thousand, it really begins to build.

As you consistently continue to invest. Through the ups in the market and the downs, you will see massive growth.

Once you become a 401(k) millionaire the sky’s the limit. Because as you cross that million-dollar mark, compound interest will be producing a significant amount of money each year.

That is why we have the 401(k) million dollar goal. To create financial freedom. The biggest way to achieve that is to max out your 401(k).

Never Take Your Money Out of Your 401(k)

One of the biggest lessons to understand as an investor is the oldest investing quote in the book. “Buy low and sell high”.

The problem is most people invest with their emotions. This can lead to a world of trouble.

As an investor, you have to expect that the stock market will have good days and bad dad days. They are expected. Sometimes, the stock market can have really bad days resulting in recessions.

These are normal as well.

Making sure you don’t panic during downturns and sell is the key. Just continue investing the same amount every single month. The consistency and discipline to stay in the market and continue investing are when you will really get ahead.

Taking money out of your 401(k) can ruin your progress.

How much should a 401(k) be worth to be a Millionaire?

Determining how much your 401(k) should be worth to be a millionaire depends on how soon you want to hit your goal. The amount of time in the market is key.

If you want to be a 401(k) Millionaire in 25 years

If your goal is to be a 401 Millionaire in 25 years, then here is how much you need to have in your 401(k) to hit your goal. Let’s assume you start at age 25 and received the average return of VTSAX at 8%:

Age 25 – $0

Age 30 – $80,959

Age 35 – $199,914

Age 40 – $374,699

Age 45 – $631,515

Age 50 – $1,008,681

The amazing takeaway here is to look at how much your 401(k) accelerates from age 45 – age 50. This is the power of compound interest. It takes some time to get going but once it does it’s like a locomotive coming down a track. This is why the average 401(k) millionaire is heading towards their golden years.

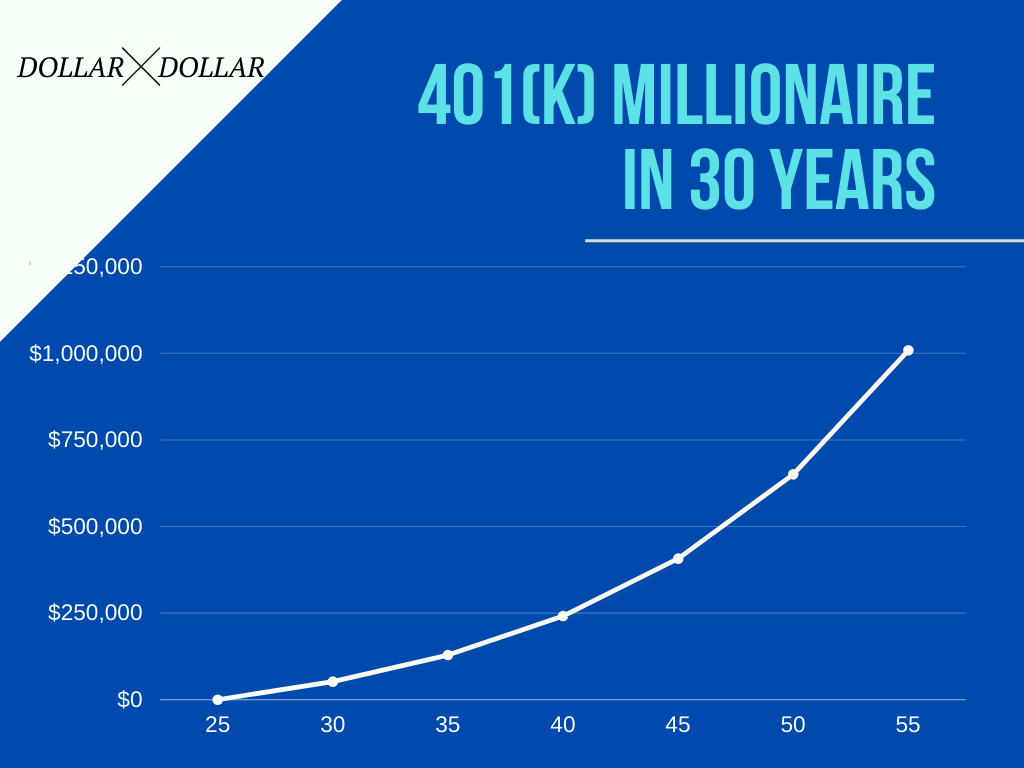

If you want to be a 401(k) Millionaire in 30 years

Becoming a 401(k) millionaire in 30 years is an easier goal to accomplish. This is because you have to save less each month to achieve that goal. Let’s again assume you start at age 25 and received the average return of VTSAX at 8%:

Age 25 – $0

Age 30 – $52,212

Age 35 – $128,930

Age 40 – $241,653

Age 45 – $407,281

Age 50 – $650,642

Age 55 – $1,008,650

The acceleration from age 50 to age 65 is astounding. Both of these examples show how important it is to throw as much money into your 401(k) as possible. Then allow compound interest to get to work.

The Average Age of a 401(k) Millionaire

The average 401(k) millionaire in America is 60 years old. And that is for good reason. They’ve had time to invest and allow their money to compound and grow.

Because you have limited funds they can contribute each year this is right on par. If you maxed out your 401(k) every single year and had an average return of 6%, you would hit millionaire status in 24 years. So, a 30 year old starting from zero would be there at 54.

Or a 22 year old would be there at 46 (see the power of starting early).

That isn’t bad. But, if you bumped that return to 8%, you would be in the seven-figure club in 21 years. Shaving 3 years off your time horizon.

How much you’ll need to save from each paycheck to become a 401(k) Millionaire

So you’re convinced you need to save and contribute to your 401(k). But, you need some actionable advice.

How much do you need to contribute to become a millionaire every paycheck?

Knowing how much to save allows you to create a plan and system. You can know if you are on track to millionaire status.

Deciding how much you need to save depends on a few factors.

- Your investment returns.

- Your Age

- When you want to retire

Retire a 401(k) Millionaire in 30 years

Let’s say you wanted to hit the million-dollar mark in 30 years. This is the easiest path to becoming a 401(K) millionaire. You have plenty of time for compound interest to do its thing. Here is what it would take every single paycheck to accomplish that.

At a 6% Interest Rate, you would need to save $1,000 a month for 30 years ($500 a paycheck)

At a 7% Interest Rate, you would need to save $892 a month for 30 years ($446 a paycheck)

At an 8% Interest Rate, you would need to save $742 a month for 30 years ($371 a paycheck)

Retire a 401(k) Millionaire in 25 years

Retiring in 25 years requires a much more aggressive savings rate. What you are buying is time, which in this case is 5 additional years. The good news is, having a million dollar 401(k) in 25 years is very doable with consistent investing.

The added bonus would be if your portfolio received a surging market, you could reach your goal even sooner.

At a 6% Interest Rate, you would need to save $1,542 a month for 25 years ($771 a paycheck)

At a 7% Interest Rate, you would need to save $1,334 a month for 25 years ($667 a paycheck)

At an 8% Interest Rate, you would need to save $1,150 a month for 25 years ($575 a paycheck)

Retire a 401(k) Millionaire in 20 years

Now, maybe you want to speed up the process. You don’t want to wait for the status symbol of choice. As you will soon see, this is very difficult to do. This is because the 401(k) has limits to how much you can contribute.

You would need higher than market average investment returns to accomplish this. This means that reaching million-dollar status in less than twenty years is not as easy.

The majority of professional fund managers can not even beat market returns consistently year over year. Let alone an average investor trying to beat returns. Here is how long it would take to be a 401(k) millionaire in 20 years.

At a 9.1% Interest Rate, you would need to save $1,625 a month for 20 years ($813 a paycheck)

At a 10% Interest Rate, you would need to save $1,500 a month for 20 years ($750 a paycheck)

At an 11% Interest Rate, you would need to save $1,250 a month for 30 years ($625 a paycheck)

The 401(k) Millionaire Chart

If you save 13,800 per year ($575 per paycheck), and wanted to be a 401(k) millionaire in 25 years here is what it would look like with an 8% return:

401(k) Millionaire in 25 Years while Adding $13,800 Per Year

If you want to work a little longer to hit the million dollar mark in 30 years here is the chart at an 8% rate. With an 8% return, you would need to save $742 a month for 30 years ($371 a paycheck). Here is the chart:

| Start Balance | Yearly Contribution | Interest | End Balance | |

| 1 | $0.00 | $13,800.00 | $498.96 | $14,298.97 |

| 2 | $14,298.97 | $13,800.00 | $1,642.87 | $29,741.86 |

| 3 | $29,741.86 | $13,800.00 | $2,878.33 | $46,420.17 |

| 4 | $46,420.17 | $13,800.00 | $4,212.59 | $64,432.76 |

| 5 | $64,432.76 | $13,800.00 | $5,653.60 | $83,886.35 |

| 6 | $83,886.35 | $13,800.00 | $7,209.89 | $104,896.23 |

| 7 | $104,896.23 | $13,800.00 | $8,890.68 | $127,586.89 |

| 8 | $127,586.89 | $13,800.00 | $10,705.93 | $152,092.81 |

| 9 | $152,092.81 | $13,800.00 | $12,666.40 | $178,559.21 |

| 10 | $178,559.21 | $13,800.00 | $14,783.70 | $207,142.91 |

| 11 | $207,142.91 | $13,800.00 | $17,070.39 | $238,013.32 |

| 12 | $238,013.32 | $13,800.00 | $19,540.03 | $271,353.35 |

| 13 | $271,353.35 | $13,800.00 | $22,207.24 | $307,360.59 |

| 14 | $307,360.59 | $13,800.00 | $25,087.81 | $346,248.41 |

| 15 | $346,248.41 | $13,800.00 | $28,198.84 | $388,247.25 |

| 16 | $388,247.25 | $13,800.00 | $31,558.76 | $433,606.00 |

| 17 | $433,606.00 | $13,800.00 | $35,187.45 | $482,593.45 |

| 18 | $482,593.45 | $13,800.00 | $39,106.44 | $535,499.89 |

| 19 | $535,499.89 | $13,800.00 | $43,338.96 | $592,638.85 |

| 20 | $592,638.85 | $13,800.00 | $47,910.08 | $654,348.93 |

| 21 | $654,348.93 | $13,800.00 | $52,846.89 | $720,995.81 |

| 22 | $720,995.81 | $13,800.00 | $58,178.63 | $792,974.45 |

| 23 | $792,974.45 | $13,800.00 | $63,936.93 | $870,711.37 |

| 24 | $870,711.37 | $13,800.00 | $70,155.87 | $954,667.25 |

| 25 | $954,667.25 | $13,800.00 | $76,872.34 | $1,045,339.60 |

401(k) Millionaire in 30 Years While Adding $8,904 Per Year

| Start Balance | Yearly Contribution | Interest | End Balance | |

| 1 | $0.00 | $8,906.00 | $321.94 | $9,225.94 |

| 2 | $9,225.94 | $8,906.00 | $1,060.04 | $19,189.96 |

| 3 | $19,189.96 | $8,906.00 | $1,857.13 | $29,951.10 |

| 4 | $29,951.10 | $8,906.00 | $2,718.06 | $41,573.14 |

| 5 | $41,573.14 | $8,906.00 | $3,647.80 | $54,124.93 |

| 6 | $54,124.93 | $8,906.00 | $4,651.93 | $67,680.87 |

| 7 | $67,680.87 | $8,906.00 | $5,736.41 | $82,321.28 |

| 8 | $82,321.28 | $8,906.00 | $6,907.66 | $98,132.93 |

| 9 | $98,132.93 | $8,906.00 | $8,172.58 | $115,209.51 |

| 10 | $115,209.51 | $8,906.00 | $9,538.71 | $133,652.21 |

| 11 | $133,652.21 | $8,906.00 | $11,014.13 | $153,570.33 |

| 12 | $153,570.33 | $8,906.00 | $12,607.59 | $175,081.90 |

| 13 | $175,081.90 | $8,906.00 | $14,328.49 | $198,314.40 |

| 14 | $198,314.40 | $8,906.00 | $16,187.10 | $223,405.49 |

| 15 | $223,405.49 | $8,906.00 | $18,194.40 | $250,503.88 |

| 16 | $250,503.88 | $8,906.00 | $20,362.26 | $279,770.13 |

| 17 | $279,770.13 | $8,906.00 | $22,703.57 | $311,377.68 |

| 18 | $311,377.68 | $8,906.00 | $25,232.16 | $345,513.84 |

| 19 | $345,513.84 | $8,906.00 | $27,963.06 | $382,380.89 |

| 20 | $382,380.89 | $8,906.00 | $30,912.42 | $422,197.31 |

| 21 | $422,197.31 | $8,906.00 | $34,097.74 | $465,199.04 |

| 22 | $465,199.04 | $8,906.00 | $37,537.84 | $511,640.90 |

| 23 | $511,640.90 | $8,906.00 | $41,253.22 | $561,798.12 |

| 24 | $561,798.12 | $8,906.00 | $45,265.81 | $615,967.91 |

| 25 | $615,967.91 | $8,906.00 | $49,599.37 | $674,471.29 |

| 26 | $674,471.29 | $8,906.00 | $54,279.65 | $737,654.94 |

| 27 | $737,654.94 | $8,906.00 | $59,334.32 | $805,893.28 |

| 28 | $805,893.28 | $8,906.00 | $64,793.42 | $879,590.68 |

| 29 | $879,590.68 | $8,906.00 | $70,689.19 | $959,183.88 |

| 30 | $959,183.88 | $8,906.00 | $77,056.65 | $1,045,144.54 |

401(k) Millionaire Success Stories (A Real World Example)

One of my favorite stories is Fritz at the retirement manifesto. I highlight Fritz because he is a wealth of information and provides extreme value on his blog.

He became a 401(k) millionaire in 28 years. He started investing in his 401(k) in 1985. He didn’t wait until it was convenient or he had more money to start investing in his 401(k), instead he started right away. There was no delay, he didn’t allow analysis paralysis to get in the way.

Starting early was a key factor in why Fritz was able to retire a millionaire

He didn’t make big money at his first job. He only made $21,500 per year, but starting early allowed Fritz to plant the seed. Because of compound interest, it allowed Fritz to start small and have big wins in the long run.

Starting early was not the only thing Fritz did right away. He also made sure to contribute enough money to get his employers to match. As we know, this is free money.

Plus, it allows you to reach your 401(k) millionaire goal even faster.

Fritz focused his time on increasing his earnings

Fritz started going above and beyond at work. If he increased his earnings, it would be much easier to save rather than trying to save on a small salary.

Every time he got a raise he would increase the amount he contributed to his 401(k). This is so he could avoid the lifestyle creep trap.

Fritz Lived Frugally and Kept His Investments Simple

Living within his means is a major factor as to why Fritz was able to join the million-dollar club. He would spend money on his values and save where he did not value. He drove old cars and maintained a frugal lifestyle even when he climbed the corporate ladder.

The key was understanding that you don’t have to invest in the latest hot stock and ride it to the moon to retire a millionaire. Instead, he invested in low-cost mutual funds, such as a target-date fund or my favorite option, and index fund.

This kept his fees at a minimum and allowed Fritz to maximize his returns.

Andrew is the host of The Personal Finance Podcast, a show that is changing the way you think about your money. His primary goal with the podcast is to bring as much value as possible to his listeners.

Andrew's favorite free financial tool he's been using since 2014 to manage his net worth is Personal Capital. Each month he uses their free Investment Checkup tool and Retirement Planner to track his investments and ensure that he's on the fast track to financial freedom.

His favorite investment platform is M1 Finance, a site that allows him to build a custom portfolio of stocks for free. It has no trading fees and is his preferred way to invest without having to lift a finger.

- Who is Eligible for an FHA Loan? - November 10, 2020

- How to Write a Check: A Step by Step Guide (With Examples) - November 6, 2020

- How to Buy Vanguard Index Funds - October 14, 2020